In a Nutshell – The Race Continues

This “In a Nutshell” follows the journey of the ASX listed Aged Care Groups and compares their half year performance.

Australia’s aged care industry continues to move into unchartered territory and providers are being faced with a myriad of challenges and opportunities. Our predictions around changing consumer choice, regulation and funding flows are now becoming reality. With growing uncertainty in the wider market, the three ASX listed residential aged care providers, Estia Health, Japara Healthcare and Regis Aged Care will need to navigate carefully to achieve investor expectations.

A previous edition of “In a Nutshell” highlighted the aggressive acquisition and expansion strategies that the listed companies have undertaken. Consolidation across the industry continues as regulatory change and increasing competition drives out underperforming providers. In combination with larger providers targeting greater market share, we continue to witness unprecedented acquisition prices for mature stock.

The release of the 2016 half year reports and financial statements by the listed companies demonstrated that this strategy is still being employed. Estia and Japara acquired a combined 14 facilities (approximately 1,200 beds) in the 6 month period. Whilst Regis did not acquire any facilities during this period, the acquisition of Masonic Care Queensland was announced shortly after the release of the half year results. This large acquisition of 6 facilities (711 places) will represent a 14% increase in Regis’s operating places. Estia’s acquisition of Kennedy Health Care was completed in February 2016, which further increases their operating places by 21% (8 facilities, 959 places).

Financial Results

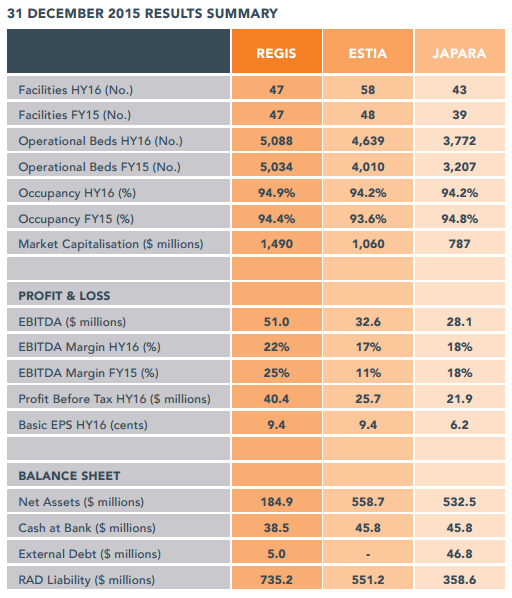

The following provides a summary and high level analysis of the 31 December 2015 results (Half Year):

Whilst positive results have been achieved by the companies, the importance of maintaining profit levels and achieving forecasted results was apparent after strong negative sentiment from Estia investors when they reported their half yearly results. Although Estia forecasted stronger results for the second half of the year, share prices have not recovered. Regis and Japara expect the second half results to be in line with first half of the year. Following the announcement of the Masonic Care Queensland acquisition, Regis’s share prices have remained steady.

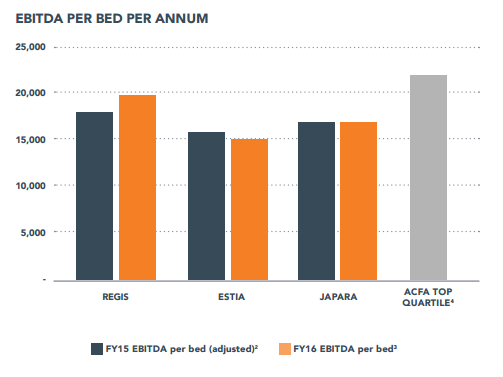

Annualised Earnings before Interest, Tax and Depreciation (EBITDA) indicate that the listed company performance is still behind the national top quartile performance based on the Aged Care Financing Authority (ACFA) data. This may present opportunities for further earnings growth as acquired homes are transitioned into the groups.

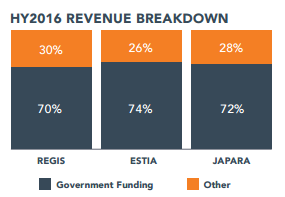

Half year revenues are presented on the right. Government funding, which primarily represents revenue from Aged Care Funding Instrument (ACFI), remains relatively comparable. However, Regis is receiving the lowest portion of government funding and highest portion of “other income”.

Resident fees are a major component of other income which can be impacted by residents’ payment preferences. While the payment preferences of Estia and Japara’s incoming residents are comparable to 30 June 2015, there has been a significant movement in Regis’ incoming residents electing to pay a combination of Refundable Accommodation Deposits (RAD) and Daily Accommodation Payments (DAP), from 25% at 30 June 2015 to 41% at 31 December 2015.

Regis stated the change in preferences “reflects the tail end of the grandfathering of residents from the impacts of the LLLB legislation”. Regis boasts a healthy balance sheet and little debt (pre Masonic acquisition) and RAD’s may have become a lower priority as the group benefits from DAP’s at rates more generous than bank interest earned on resident deposits.

All three companies are clearly driven to increase their market share. We continue to see strong interest from investors to acquire existing stock, however, the number of homes available for sale is declining.

Based on the pipeline of developments, it is evident that greenfield developments will be fuelling organic growth. These developments are key in meeting the estimated 74,000 additional beds required across Australia over the next decade. The Government process for the allocation of places (Aged Care Approval Rounds ACAR)) to facilitate new development saw Regis and Japara receiving a large number of places earlier this year. In addition to places allocated in previous rounds and offline licences, these companies have sufficient places to meet their immediate brownfield and greenfield development requirements.

Estia’s current pipeline and low ACAR allocation leaves them around 3,000 places short of meeting their 10,000 bed target by 2020. Given the longer time frame associated with brownfield and greenfield developments, the three listed companies and other large providers will continue to look for acquisition opportunities to grow their presence.

The Coalition Government has repeatedly questioned the benefits of continuing Australia’s managed supply program and is promoting a conversation around the cessation of ACAR for residential aged care. How this would look and the impact of these reforms on the industry are discussions we will begin to hear more of in the near future and will be the topic of our next “In a Nutshell” edition.

In the meantime, the aged care industry will continue to evolve in response to changes in regulation and consumer needs. We will watch with interest as the listed groups navigate through the next wave of change as well as meeting investor expectations.